Submitted by International Review on

As far as the economy is concerned, the whole world seems to be hanging on one question: will there be a recovery in the United States? Does the locomotive that has drawn the world economy for two decades have the strength to start up one more time?

The answer given by the economists is clear: "yes", they say. Their job as managers and spokesmen of capitalist ideology forbids them to think otherwise, whatever the situation. The one thing they do not doubt is that capitalism is eternal; that there can be nothing beyond the realm of the market and the exploitation of wage labor. Even the most cynical and clear-sighted of them can see in the most serious difficulties of the international, capitalist economy nothing more than transient contradictions, upsets caused by "the needs of progress", that can be easily overcome by making possible the "necessary structural changes". From this point of view, the present open recession which started to hit the main economic powers of the world more than a year ago, is nothing more than a "cyclical slowing down"; a natural and healthy contraction following an over-long period of expansion.

"The whole world economy is in the process of purging itself after its years of excess", said Raymond Barre[1] in February 1992, at the Davos Forum on the world economy.

George Bush and the team responsible for organizing his current electoral campaign in the United States went further: the recession was coming to an end, the recovery was under way. "The old adage is coming true: As housing goes, so goes the economy", said Bush in the middle of May, quoting statistics to show an increase in house building in the United States during the first months of 1992.

But historic reality scoffs at the dreams and wishes of those 'in charge of' the established order. A few days after this optimistic declaration from Bush, the official figures showed a decline of 17% in the indices for the construction of new houses, the most dramatic drop for eight years! The difficulties that the world bourgeoisie is experiencing in trying to cope with the present open recession in its economy are qualitatively new. This recession is not like previous ones.

Recession become more and more destructive

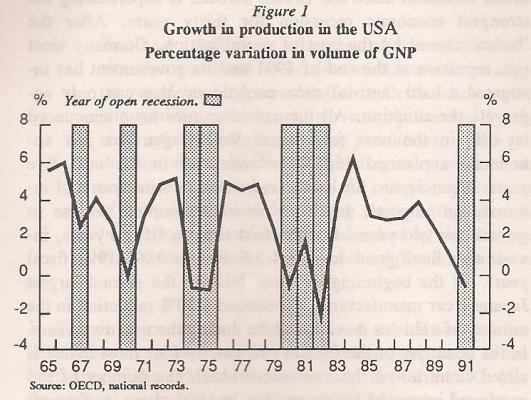

It is true that for two decades the world economy, following to varying degrees the different movements of the American economy, has gone through a succession of recessions and 'recoveries'. But since the end of the 60s or, in other words, since the end of the period of 'prosperity' owing to reconstruction after the second world war, the recessions haven't followed a cyclical movement that can be likened to the breathing of a healthy body. They have even less in common with the rhythm of capitalism's cyclical crises in the second half of the nineteenth century, when the system was at the height of its ascendant period; then their intensity diminished every ten years. The fluctuations of the world economy over the last twenty years don't express the cyclical movement of an expanding, vital system; but the convulsions of a body that is becoming sicker and sicker. Since the recession of 1967, each dive is deeper and longer-lasting that the one before. The fluctuations in the growth of production in the United States, the heart of world capitalism, speak volumes on this (see the graph below).

This 'electro-cardiogram' of capitalism's heart gives only a partial picture of reality. In fact there has not been a real recovery of economic growth internationally since the recession of 1980-1982. The countries of the 'third world' have not really managed to pick up. For most of the underdeveloped countries, the 1980s are synonymous with the greatest economic stagnation ever experienced. The African continent, a large part of Asia and Latin America were devastated economically in this period. From the middle of this decade, the ex-USSR and the countries under its influence plunged into a chaos that found expression in one of the most brutal economic recessions ever known. It is only in a small part of the world, comprising the most industrialized countries of the old western bloc, that the economy has undergone any development at all throughout the 1980s. What's more, this development has only been in certain areas even in these countries: in this period regions which were among the first on the planet to be industrialized: Great Britain, France, Belgium or the United States, for example, are being turned into industrial wastelands.

So the recession that is hitting the most industrialized countries today has nothing to do with a healthy breathing-space in the course of world-wide growth. On the contrary, it marks the collapse of the only part of the world that up to now has managed to escape the general stagnation to some extent.

The motor for 'restarting' the economy no longer fires

But are the economies of the most industrialized countries able to achieve some small degree of growth even in their sickness, as they have done in previous recessions? Are the governments of the big powers able to restart the motor once more, by lowering interest rates and printing money? Can the flight into credit, the attitude, 'produce today; pay tomorrow', still enable them to trick their way out, by deferring payment on the bills?

The bureaucracy of the OECD, who so extol the virtues of an eternal capitalist system and the victory of 'liberalism', announced the imminent arrival of a 'moderate recovery' at the end of 1991[2]. But this 'forecast' was accompanied by a significant reservation:

"In most of the important countries, the lethargy in monetary growth is both involuntary and unusual... The persistent contraction in the offer of bank credits, which seems to lie at the origin of this slow down, could offer a threat to growth... The uncertainty due to the present slowing down of monetary growth poses a very difficult problem for those in a position of responsibility."

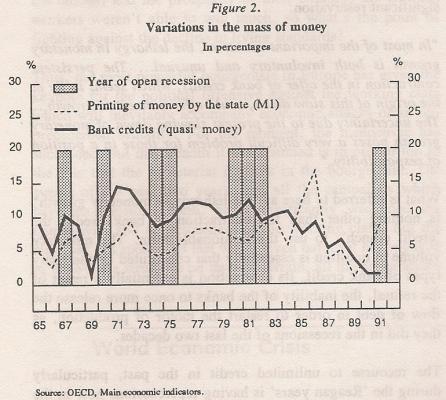

What is referred to here as "the lethargy in monetary growth" is nothing other than the contraction in bank credit, the 'credit crunch', to use the fashionable term. The monetary volume in question is essentially that constituted by the many types of bank credit. Its contraction is essentially a result of the refusal, the inability of the banks to once more release the flow of debt in order to restart the motor of production, as they did in the recessions of the last two decades.

The recourse to unlimited credit in the past, particularly during the 'Reagan years' is having repercussions now in the form of bankruptcies. The growing insolvency of companies, and of a large number of banks, makes it impossible to obtain repayment on an increasing amount of credit; this pushes more banks to the brink of bankruptcy every day. The collapse of the American savings banks at the end of the 1980s was only the beginning of this stagnation[3]. Given this situation, the banks use the new credit facilities created by the state (lowering interest rates, printing money), not to make more credit available, but to try to refill their coffers and reduce the imbalance in their accounts.

In 1991, Lowell L. Bryan, a 'well-known American expert' of the banking and financial system, stated in a book with the evocative title 'Bankrupt'[4]: "Perhaps as much as 25% of the [American] banking system, representing well over $750 billion[5] in assets has begun to post such massive loan losses that it has no choice but to focus on credit collection, rather than credit extension... Moreover, the banks without credit problems naturally get more cautious as well."

Figure 2 (on the following page) show clearly that there really is an unprecedented collapse in the growth of the volume of bank credit (especially since 1990). It also shows the government's present inability to restart the credit machine. Unlike the recessions of 1967, 1970, 1974-75, 1980-82, the increase in monetary volume created directly by the state (notes issued by the central bank and coins) no longer produces an increase in the volume of bank credits. The American government has put its foot down hard on the accelerator, the banking machine has not responded.

"We have created a market place that is efficient in the destruction of our economy. Our financial system is close to breaking down. Our regulation of our financial system, and the social contract that underlines it, is bankrupt", so the author of 'Bankrupt' affirms bitterly. And this affirmation sums up precisely what it is that makes this open recession different from the others.

The world economy is not experiencing a process of financial 'cleansing', but rather the destructive consequences of the longest period of speculation in the history of capitalism. The motor that, for years, has made it possible for it to postpone its problems, is now in pieces; and the fundamental problem, capitalism's inability to create its own outlets, has not been solved in any way all. Quite the reverse. Never has the gap between what society is able to produce and what it can sell been so great[6].

Still more unemployment and misery

Superficially, the massive doses of monetary intervention by the present Bush administration - their hand forced by the prospect of the presidential elections - could slow down the decline in specific sectors. For example, the recent shower of interest rate reductions by the Federal Reserve (more than twenty in a few months), has managed to check the fall in house building temporarily. But all this is on a very fragile basis.

The desperate attempts of the American government to limit the damage on the eve of the elections, will at best succeed in slowing down the decline temporarily. But this will not produce a real recovery or the end of the recession. At the most it will deflect the downward spiral momentarily, producing a 'double dip' recession, like the one of 1980-1982, which was interrupted by an artificial recovery in 1981 (see figure 1).

The top American companies, like General Motors, IBM or Boeing, continue to lay off workers. Their plans for 'reconstruction' predict tens of thousands of job losses (74,000 for General Motors alone) and are forecast to continue for the next three to five years. This speaks volumes about the confidence of the managers of the big international companies in the possibility of recovery.

The changes in the economies of the other big industrialized countries confirm the dynamic of the reflux. The United Kingdom continues to sink into what is already the most brutal recession since the 1930s. Sweden is experiencing the strongest economic recession for thirty years. After the 'boom' caused by the cost of re-unification, Germany went into recession at the end of 1991 and its government has instigated a hard 'anti-inflation cool down' that can only aggravate the situation. All the car companies have announced lay-offs in the next few years: Volkswagen has just announced a planned 15,000 redundancies in the next five years. Even Japan, hit by the reduction in American and international imports, has seen an uninterrupted decline in growth for two years. For the first time in fifteen years, investments have gone down (-4.5% for the 1991-1992 fiscal year). At the beginning of June, Nissan, the second largest Japanese car manufacturer, announced a 30% reduction in the number of vehicles it will produce during the next two years. In the countries of the OECD (the twenty-four most industrialized countries of the ex-western bloc), the number of unemployed increased by six million in 1991 alone, and no official forecast dare predict a real end to the hemorrhage.

****

For the international working class, for the exploited of the world, this recession is also not like previous ones. The new intensification of unemployment and misery, which is hitting, and will continue to hit the working class in the years to come, is also making itself felt in an unprecedented way. In addition, these blows are raining down on a class which suffered, throughout the 80s, the most violent economic attack since the last world war. Today, it is the central sectors of the world working class, those in the most industrialized countries, those who have so far been the least hard-hit, who find themselves in the front line. In this way, this new eruption of difficulties for the capitalist system once more places the revolutionary class before its historic responsibilities. RV, 10/6/92

[1] "The foremost economist of France", Giscard d'Estaing said of this old leader of the French government.

[2] Economic Perspectives no.50, December 1991.

[3] See the article, 'The credit crisis and the impossibility of any recovery: a recession that gets deeper and deeper, in the International Review no.68.

[4] 'Bankrupt - Restoring the health and profitability of our banking System', Harper Collins Publishers.

[5] This is equivalent to the total production of Spain and Switzerland in 1991.

[6] In May 1992, the world press published two items of news simultaneously: the United Nations announced that 60 million human beings are in danger of dying of starvation in Africa this year, and the EEC gave notification of its decision to make 15% of the cereal land in Europe barren, because of lack of buyers!

del.icio.us

del.icio.us Digg

Digg Newskicks

Newskicks Ping This!

Ping This! Favorite on Technorati

Favorite on Technorati Blinklist

Blinklist Furl

Furl Mister Wong

Mister Wong Mixx

Mixx Newsvine

Newsvine StumbleUpon

StumbleUpon Viadeo

Viadeo Icerocket

Icerocket Yahoo

Yahoo identi.ca

identi.ca Google+

Google+ Reddit

Reddit SlashDot

SlashDot Twitter

Twitter Box

Box Diigo

Diigo Facebook

Facebook Google

Google LinkedIn

LinkedIn MySpace

MySpace